You’re about to make one of the most important hiring decisions in your syndication journey. Choosing the wrong PPM lawyer doesn’t just cost you money—it can sink your entire deal. But here’s what most syndicators don’t realize: not all securities attorneys are created equal. The difference between a generalist and a true specialist can mean the difference between closing your raise or watching investors walk. What separates the two might surprise you.

I’m Tilden Moschetti, and I’ve been on both sides of the table—as a syndicator raising capital and as the attorney drafting the documents. That dual perspective shapes everything I do for my clients. Let me tell you why it matters.

Key Takeaways

- Hire a PPM lawyer with real syndication experience, as they understand investor psychology and draft documents that build confidence rather than create friction.

- Specialized Reg D attorneys deliver documents faster, often within days, while generalists may take six to eight weeks, risking deal momentum.

- Flat-fee structures eliminate billing anxiety, provide cost predictability, and keep attorneys focused on quality rather than maximizing billable hours.

- A specialized attorney deeply understands 506(b) and 506(c) distinctions, preventing costly exemption mistakes that could trigger securities law violations.

- Building a long-term relationship with your PPM lawyer creates institutional knowledge that streamlines future offerings and anticipates regulatory complexities.

Why Your PPM Lawyer Must Be a Syndicator First (The “Boots on the Ground” Advantage)

When you hire a PPM lawyer who’s never actually syndicated a deal, you’re getting legal documents drafted, like a private placement memorandum, by someone who’s never sat across the table from a skeptical investor and had to earn that check.

That gap matters—because the language that protects your promote, structures your fees, and builds investor confidence isn’t purely theoretical; it’s forged from real experience closing real deals.

Your attorney needs to know what actually gets investors to sign, not just what satisfies an SEC filing requirement.

From Litigation Battlefields to Building Wealth: My Path to Syndication Law

I spent ten years as a litigator waging bloody battles over property-centric disputes. Partner disputes. Bankruptcies. Divorces. Every variation of conflict you can imagine where real estate was at the center.

I hated it.

Not because I wasn’t good at it—I was. But litigation destroys value. Every time. Two partners who built a $10 million portfolio together would spend $500,000 in legal fees fighting over the carcass while the properties deteriorated from neglect. Divorcing couples would torch their rental portfolios rather than see their ex-spouse benefit. Bankruptcy proceedings would grind profitable developments into dust.

I watched smart people spend hundreds of thousands of dollars arguing over ambiguous contracts that should have protected them. I realized I didn’t want to litigate broken deals; I wanted to build bulletproof ones.

So I pivoted.

My very first syndication deal was a triple-net medical office building being developed outside Sacramento. It took me six months to put together—not because the deal was complicated, but because I had to learn the “alphabet soup” of SEC regulations from scratch. Rule 506(b). Rule 506(c). Regulation D. Form D filings. Blue Sky laws. Accredited investor verification requirements.

I made every mistake a first-time syndicator makes. I nearly blew the pre-existing relationship requirements by mentioning the deal too early to someone I’d just met at a conference. I had to rewrite my waterfall provisions three times because the first two versions were ambiguous enough to cause exactly the kind of disputes I’d spent a decade litigating.

But I closed that deal. And something clicked.

I realized I could use my legal expertise to help sponsors build wealth instead of tearing it down. Every PPM I draft now, every operating agreement I structure, every subscription document I produce—it’s designed to create value and protect the people creating it. That’s a fundamentally different mission than litigation, and I’ve never looked back.

The Danger of “Desk Attorneys”

Many PPM lawyers have never raised a dollar of investor capital in their lives—and that’s a serious problem.

They draft documents from a theoretical framework, not from real-world experience. They’ve never sat across from a skeptical investor, never navigated a live deal structure, and never felt the pressure of a closing deadline with capital commitments on the line.

That gap shows in their work.

When your attorney hasn’t personally syndicated deals, they miss the practical nuances that matter—how investors actually read disclosures, where deal structures break down, and what language creates friction versus confidence.

I’ve seen desk attorneys draft risk disclosures that read like academic exercises—technically comprehensive but so dense that investors’ eyes glaze over by page three. The risk factors are there, but they’re buried in language that screams “I’m covering my liability” rather than “I’m helping you make an informed decision.”

Real investors notice the difference. Sophisticated accredited investors have seen hundreds of PPMs. They know when a document was drafted by someone who understands the business versus someone who just understands the regulations.

Sitting Across the Table: What Actually Gets the Check Signed

There’s a reason the best PPM lawyers aren’t just lawyers—they’re syndicators. They’ve sat across the table from investors. They’ve answered hard questions in real time. They know what gets a check signed—and what kills a deal.

When your attorney has personally raised capital, structured deals, and navigated investor objections, they’re not just drafting documents. They’re building legal frameworks that actually support your raise.

I don’t just advise syndicators—I am one. That experience shapes every PPM, operating agreement, and subscription document I produce.

I understand the investor psychology behind the disclosures, not just the legal requirement to include them.

That’s the “boots on the ground” advantage. You’re not getting theory. You’re getting someone who’s done exactly what you’re trying to do.

Protecting Your Promote (Because I Protect My Own)

Your promote is the whole point—it’s why you structured the deal, why you did the work, and why you took the risk. A lawyer who’s never syndicated doesn’t feel that the way you do.

I’ve sat in your seat. I’ve built my own promotes, defended them in negotiations, and watched vague PPM language erode them later. That experience changes how I draft your documents.

Let me give you a real example of how this plays out.

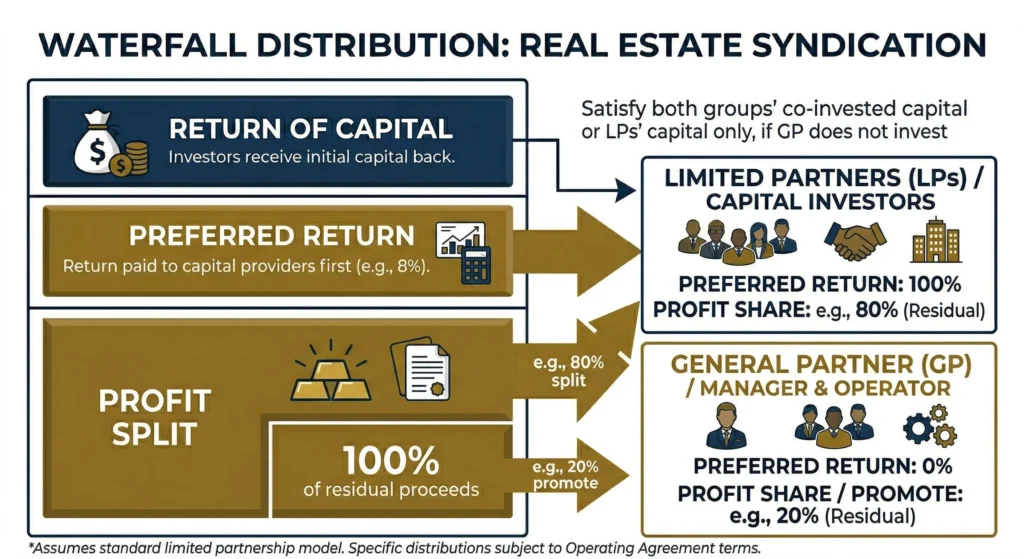

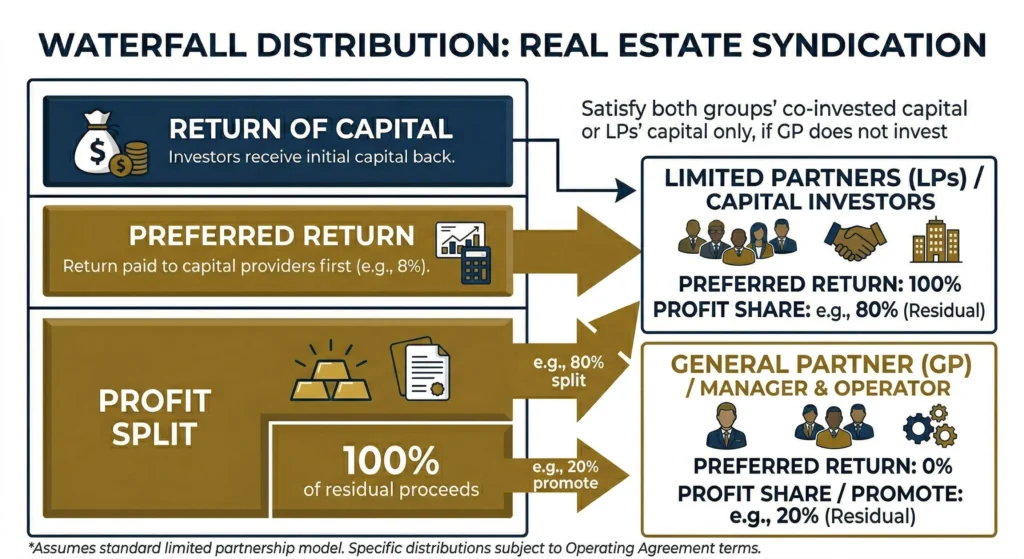

I once reviewed a PPM drafted by a generalist attorney for a multifamily syndicator. The preferred return provision stated that investors would receive “an 8% preferred return on their capital contribution before any distributions to the sponsor.”

Sounds straightforward, right?

But here’s what the language didn’t specify: Was the 8% calculated on unreturned capital or original capital? Was it cumulative or non-cumulative? Did it accrue during periods when no distributions were made?

The sponsor assumed the preferred return was calculated on unreturned capital—so once investors got some of their principal back, the preferred return base would decrease. The investors read it as original capital—meaning the 8% was always calculated on their initial investment, regardless of distributions.

When the property sold and the waterfall kicked in, that ambiguity cost the sponsor nearly $340,000 in promote that he believed he’d earned. The language technically supported both interpretations, and rather than litigate, he settled.

That’s not a hypothetical. That’s what happens when your PPM lawyer doesn’t understand how waterfalls actually work in practice, not just on paper.

When your waterfall provisions are ambiguous, your promote gets squeezed. When your preferred return calculations aren’t airtight, investors push back—and win. When your promote structure isn’t clearly defined, disputes follow.

I draft PPMs that protect your promote because I protect my own the same way. That’s not a marketing line. That’s the difference between a lawyer who studies syndications and one who runs them.

Generalists vs. Specialists: Why I Only Draft Regulation D Offerings

When you hire a law firm that handles everything from divorces to tax disputes to real estate closings, you’re paying for breadth at the expense of depth.

I’m not your real estate lawyer, your tax advisor, or your family law attorney—I draft Regulation D offerings, full stop.

That singular focus means you get an attorney whose entire practice lives inside 506(b) and 506(c), not someone who picks up a PPM between client matters.

The Hidden Cost of the “We Do It All” Law Firm

Regulation D compliance isn’t something you want a part-time practitioner handling.

Mistakes in your PPM—missing risk factors, improper exemption reliance, or weak offering disclosures—can expose you to securities fraud claims and regulatory action.

Here’s a scenario I see far too often: A sponsor goes to their “trusted business attorney”—the same lawyer who helped them form their LLC and reviewed their office lease. The attorney says, “Sure, I can do your PPM. I took a securities law course in law school.”

Six weeks later, the sponsor has a document that technically contains the required disclosures but relies on Rule 506(c) when the sponsor’s entire investor network consists of pre-existing relationships who could have participated under 506(b). The attorney never thought to ask about the marketing strategy because they don’t think about investor funnels—they think about legal compliance in a vacuum.

Now the sponsor is locked into verifying every investor’s accredited status through third-party documentation or CPA/attorney letters, when they could have simply accepted self-certification from investors they’ve known for years.

That’s not just inefficient—it’s insulting to long-standing investor relationships. “Hey, Tom, I know we’ve invested together three times, but this new lawyer needs you to send me two years of tax returns to prove you’re accredited.”

When you hire a specialist, you’re not paying for breadth. You’re paying for depth—and in a capital raise, depth is exactly what keeps you legally protected and your investor relationships intact.

Deep Expertise in 506(b) and 506(c) Exclusivity

There are exactly two Regulation D exemptions serious capital raisers rely on: Rule 506(b) and Rule 506(c). Most attorneys treat these as side items on a broader menu. I don’t. This is the work I do exclusively.

506(b) lets you raise from up to 35 non-accredited investors in any 90-day period but bans general solicitation. 506(c) flips that—you can publicly advertise, but every investor must be verified accredited. The tradeoffs aren’t subtle. Choose the wrong exemption, and you’ve either violated securities law or locked yourself out of your best investors.

The distinction matters in ways that generalists completely miss.

I recently consulted with a sponsor who had been advised by a generalist to run a 506(c) offering because “it’s simpler—you can just advertise.” The sponsor had a podcast with about 8,000 listeners and figured he’d promote the deal there.

But here’s the problem: His podcast audience included plenty of non-accredited listeners who’d been following him for years. These were exactly the sophisticated but non-accredited investors who could have participated under 506(b). The generalist’s advice eliminated 95% of his potential investor pool in exchange for the ability to advertise to people he didn’t know.

Worse, the sponsor had mentioned a previous deal casually on the podcast before engaging me. Nothing specific—just “I’ve got something interesting in the pipeline.” Under 506(b), that kind of general statement might have been acceptable as long as no specific deal terms were discussed. But the generalist had already filed Form D for a 506(c) offering. The sponsor was now locked in.

If it feels like you’re broadcasting your deal to the world, it’s probably general solicitation and not allowed under 506(b). But if your strength is your relationship network, 506(c) might be the wrong tool entirely.

Because I focus entirely on Regulation D offerings, I’ve built deep pattern recognition around these rules. You’re not getting a generalist who occasionally drafts a PPM. You’re getting someone who lives in this space daily and can guide you to the right exemption before you make an irreversible choice.

The 2-Week Turnaround: How a Specialized PPM Lawyer Saves Your Deal

When you’re raising capital, time is your most valuable asset—investor enthusiasm fades fast, and deals that stall beyond two weeks often fall apart entirely.

A specialized PPM lawyer who drafts Regulation D offerings exclusively has developed the depth of expertise to deliver your complete document package in a fraction of the time a generalist requires. This isn’t about automation or templates—it’s about an attorney who has seen hundreds of deal structures and knows exactly how to craft yours without wasted motion.

Deal Heat Dies After 14 Days

Investor enthusiasm has a shelf life, and it’s shorter than most syndicators expect—typically around two weeks. After that window closes, momentum fades. Investors move on, redirect their capital, or simply lose confidence in your ability to execute.

You can’t blame them—hesitation signals inexperience. That’s why your PPM attorney’s turnaround time isn’t just an administrative detail. It’s a deal variable.

I’ve watched sponsors lose $2 million raises because their attorney took eight weeks to deliver documents. By week three, the anchor investor who’d committed $500,000 got cold feet. “If you can’t get your documents together, how are you going to manage my money?” By week six, two more investors had allocated their capital elsewhere. By week eight, when the documents finally arrived, the sponsor was starting from scratch with a fraction of his original momentum.

A generalist lawyer juggling unrelated cases can take six to eight weeks to deliver your documents. By then, your deal is cold and your investors are gone.

A specialized PPM lawyer understands this pressure intimately. My entire practice is built around the reality that your capital raise has a shelf life.

When you’re racing that two-week clock, you need someone who treats urgency as a baseline, not an exception.

Why Hyper-Specialization Creates Speed

Speed in legal work isn’t magic—and it certainly isn’t automation. It’s the byproduct of relentless focus on a single area of law.

When an attorney has drafted hundreds of PPMs, operating agreements, and subscription agreements, they’re not learning on your deal. They’ve internalized the patterns, the pitfalls, and the precise language that protects sponsors in every scenario.

That’s why I can deliver faster than a generalist without cutting corners—because I’m not figuring out your deal structure for the first time. I’ve lived it. I’m in the weeds on every engagement, custom-crafting your specific waterfall, your specific risk factors, your specific investor protections.

Multifamily value-add with a 70/30 split and 8% pref? I’ve drafted that structure dozens of times—and I know exactly where the ambiguities hide that will cost you your promote three years from now. Ground-up development with a promote that kicks in only after a 12% IRR hurdle? I built that waterfall last month and can tell you precisely which calculations need to be spelled out to avoid disputes. Debt fund with quarterly redemption windows and a 2/20 fee structure? I know the investor objections before you hear them.

A generalist attorney learns your deal structure while billing you. I already know it—because this is all I do.

The result? Your complete PPM package—Private Placement Memorandum, Operating Agreement, Subscription Agreement—gets delivered faster and tighter, without the costly back-and-forth that kills momentum when deal heat is already fading. Every document is custom-built for your specific deal, not adapted from a generic template.

Flat-Fee Certainty vs. Hourly Billing Agony

That expertise-driven speed also comes with a financial upside you can’t get from an hourly biller—cost predictability.

When a Reg D attorney charges by the hour, every revision, every question, every back-and-forth email becomes a line item on your invoice. You’re constantly guessing what the final bill looks like. And here’s the dirty secret of hourly billing: there’s no incentive for the attorney to be efficient. The longer your deal takes, the more they make.

A flat-fee model eliminates that anxiety entirely.

My fee structure is transparent: $15,000 for your first engagement, covering the complete PPM package—Private Placement Memorandum, Operating Agreement, and Subscription Agreement. For repeat business, that drops to $10,000.

No surprises. No billing creep. No incentive for me to slow-walk the process.

Think about what that means for your risk profile. With an hourly attorney charging $500-$750 per hour, a “simple” PPM can easily balloon to $20,000 or $30,000 by the time you’ve incorporated feedback, revised the waterfall structure, and responded to investor questions. You won’t know the final number until the invoice arrives.

With flat-fee pricing, you know the number upfront. You can budget accurately, plan your raise timeline, and focus on finding investors instead of watching the clock tick on someone else’s hourly rate.

That certainty matters when you’re racing toward a capital raise. Every dollar you save on legal fees is a dollar that can go toward acquisition costs, investor returns, or reserves.

And here’s the real kicker: when syndication is executed properly, the syndicator doesn’t pay for any of the expenses associated with forming the syndication and getting it to the funding point. The cost of the PPM and related contracts are business expenses that should be passed on to investors. It’s in investors’ interests to legally bulletproof their investment, so there’s no “convincing” required. That’s the golden standard—the cost of earning ROI through your project.

My ROI is Your Success: Building a Repeat-Business Partnership

When you hire a specialized PPM lawyer, you’re not just closing one deal—you’re building a partnership designed to scale your entire portfolio from Fund I to Fund IV and beyond.

A good Reg D attorney structures your deals with growth in mind, so each successive fund gets faster, cleaner, and more capital-efficient.

Simply put, if you don’t raise the capital, your attorney loses their best repeat client, which means their success is directly tied to yours.

I Don’t Want One Deal; I Want Your Entire Empire

A great Reg D attorney isn’t just thinking about closing your current deal—they’re thinking about your next five.

I want to understand your full capital-raising vision, whether that’s a single syndication or an entire portfolio of debt funds and equity structures.

When I invest time learning your business model, I’m building a foundation that makes every future deal faster, cheaper, and cleaner. I already know your investor base, your risk tolerance, and your compliance history.

That institutional knowledge compounds over time.

You’re not re-explaining yourself from scratch with every new offering. I anticipate your needs, flag regulatory issues before they become problems, and structure each deal to support what comes next.

One of my clients started with a single 24-unit apartment building raise—$1.2 million. Today, four years later, he’s launching his fourth fund with a $15 million target. His legal costs per dollar raised have dropped by 60% because we’re not reinventing the wheel. His investor onboarding is streamlined because I’ve refined his subscription documents based on feedback from his actual investor base. His compliance is bulletproof because I’ve tracked his entire regulatory history.

I don’t want a transaction—I want your empire.

Structuring for Scale (From Fund I to Fund IV)

Scaling from Fund I to Fund IV isn’t just about raising more capital—it’s about building a legal architecture that compounds in efficiency with every new offering.

Each fund you launch builds on the last—refined operating agreements, seasoned investor disclosures, and tighter compliance protocols. Your Reg D attorney shouldn’t be relearning your business with every engagement. They should already know your investor profile, your deal flow, and your risk tolerance.

As your fund evolves, so do the structural complexities—debt funds, equity funds, hybrid structures, and multi-vehicle strategies each carry distinct SEC compliance requirements.

A lawyer who’s tracked your growth anticipates those pivots. You’re not paying for orientation every time. You’re paying for execution.

That’s where the real ROI lives—in the institutional knowledge your attorney carries forward with you.

If You Don’t Raise the Capital, I Lose My Best Client

There’s a reason the best Reg D attorneys aren’t just service providers—they’re invested in your outcome.

If you don’t raise capital, you don’t close deals. If you don’t close deals, you don’t come back. It’s that simple.

A Reg D attorney who understands syndication knows their business model depends on yours working. That alignment matters.

I’m not drafting your PPM in a vacuum—I’m structuring it to withstand SEC scrutiny, attract sophisticated investors, and support your raise from Fund I through Fund IV.

When your attorney treats your capital raise as a shared mission, you get sharper documents, faster turnaround, and real strategic input.

That’s not a bonus—that’s the standard you should expect from anyone you hire to protect your syndication.

From Pitch Deck to PPM: Evaluating Your PPM Lawyer’s Marketing IQ

Your pitch deck tells investors a compelling story, but your PPM locks that story into a legal framework—and if your attorney doesn’t understand marketing, that framework can quietly strangle your narrative.

The choice between Rule 506(b) and 506(c) isn’t just a legal decision; it’s a marketing decision that determines whether you can publicly advertise your deal or must rely on pre-existing relationships, shaping your entire investor funnel.

Before you hire a securities attorney, you need to ask three critical questions that reveal whether they grasp the business reality behind the legal documents they’re drafting.

A Compliant PPM is Useless if it Kills Your Marketing Narrative

A technically compliant PPM that buries your investment thesis under layers of legalese isn’t protecting you—it’s sabotaging you.

Compliance and clarity aren’t mutually exclusive—they’re both required.

Your PPM needs to accurately disclose risks while still communicating why this deal is worth an investor’s capital. If your attorney doesn’t understand that balance, you’re left with a document that checks every legal box but kills investor confidence before the wire transfer conversation even starts.

Think of your PPM as your final sales document. Everything you’ve told investors verbally doesn’t count until they see it on paper. Sophisticated, accredited investors judge your deal by the quality of the PPM. A five-star legal document prepared by an experienced syndication attorney reassures them that you are the real deal.

This becomes especially critical when you’re operating under Rule 506(c), where general solicitation is permitted and your PPM works alongside public marketing materials. If your marketing says “exceptional opportunity” and your PPM reads like a 47-page warning label, you’ve created dissonance that makes investors nervous.

Under 506(b), where you can’t advertise, your PPM carries even more persuasive weight. It’s doing the heavy lifting of both legal protection and investment positioning.

A good Reg D attorney protects your raise—not just your liability.

Navigating General Solicitation (506b vs 506c Funnels)

Whether you’re raising under Rule 506(b) or 506(c) determines everything about how you market your deal—and your PPM attorney needs to understand that distinction at a strategic level, not just a technical one.

Under 506(b), you can’t generally solicit. That means no social media posts about the offering, no public webinars walking through deal terms, no broad outreach to people you don’t already have relationships with. Your relationships must come first, and your attorney should help you build a compliant pre-existing relationship funnel before money is ever discussed.

This is where I see sponsors get burned constantly. They attend a real estate conference, collect 50 business cards, and two weeks later blast an email about their new deal. That’s general solicitation to people without pre-existing relationships—and it can blow up your entire 506(b) exemption.

The line is subtle but critical: Talking about your company is one thing. Talking about your current 506(b) offering is another. When in doubt, assume it’s general solicitation and either don’t do it or switch to 506(c).

Under 506(c), you can advertise openly—but every investor must be verified as accredited through third-party confirmation. That means tax returns, CPA letters, attorney confirmations, or broker-dealer verification. Self-certification isn’t enough.

These aren’t interchangeable paths. Each requires a different marketing infrastructure, a different investor onboarding sequence, and different compliance triggers. Your attorney should be guiding that entire funnel, not just drafting documents at the end of it.

The 3 Questions You Must Ask Any Securities Attorney Before Hiring

Knowing the difference between 506(b) and 506(c) is one thing—finding an attorney who can actually execute on that knowledge is another.

Before you hire anyone, ask these three questions:

“Do you personally invest in syndications?” An attorney who’s been a limited partner understands investor psychology in ways a purely transactional lawyer never will. They know what disclosures actually matter to investors, what language creates confidence versus anxiety, and how investors actually read these documents—not how they theoretically should read them.

“How do you structure marketing funnels for 506(b) versus 506(c)?” If they can’t explain the compliance boundaries around social media, general solicitation, and pre-existing relationships without pulling out a textbook, walk away. You need someone who lives this daily, not someone who has to research your question.

“Have you drafted PPMs for deals similar to mine?” Asset class matters. A lawyer experienced in multifamily syndications thinks differently than one who’s only handled private equity funds. A ground-up development PPM has different risk factors than a stabilized cash-flowing property. Medical office buildings have different regulatory considerations than retail centers. Experience in your specific space means fewer revision cycles and better protection.

Their answers will tell you everything about whether they’re a true syndication attorney or just a securities generalist.

Common PPM Mistakes That Kill Deals (And How to Avoid Them)

I’ve reviewed hundreds of PPMs drafted by other attorneys, and certain mistakes appear over and over again. These aren’t theoretical concerns—they’re the specific issues that trigger investor lawsuits, regulatory scrutiny, and deal failures.

Vague Waterfall Language

The waterfall is where your economics live. Ambiguous language here doesn’t just create confusion—it creates litigation.

I once reviewed a PPM where the promote structure stated the sponsor would receive “20% of profits after investors receive their preferred return and return of capital.”

Sounds clear, right?

But the document didn’t define “profits.” Did it mean cash-on-cash distributions? Total return including appreciation? Net of operating expenses or gross? Did capital improvements count against profits or get capitalized separately?

The sponsor and a major investor had completely different interpretations. When the property sold, the sponsor believed he’d earned a $180,000 promote. The investor believed the promote was closer to $95,000 based on his reading of “profits.”

They settled for $140,000 after $30,000 in legal fees on both sides. The sponsor “won” but lost months of time and a key investor relationship.

Proper PPM drafting defines every term with surgical precision. There should be zero room for interpretation on the economics.

Improper 506(b) General Solicitation

This is the mistake I see most often, and it’s potentially fatal to your entire offering.

A sponsor builds a great track record, starts a podcast, and mentions that “investors who want to get involved in our next deal should reach out.” That’s general solicitation. Under 506(b), it can invalidate your exemption retroactively.

Or a sponsor posts on LinkedIn about “an exciting new opportunity for accredited investors.” General solicitation.

Or a sponsor does a “friends and family” webinar but forgets to lock registration to people with pre-existing relationships. General solicitation.

The consequences aren’t just regulatory. If your exemption is invalid, every investor in your deal may have rescission rights—meaning they can demand their capital back at any time, regardless of whether the investment has performed well. That’s an existential threat to your syndication.

Inadequate Risk Disclosures

Your risk factors section isn’t a liability CYA exercise—it’s your primary protection against investor lawsuits.

The standard is “material disclosure.” You must disclose any risk that a reasonable investor would consider important in making their investment decision.

I’ve seen PPMs that disclose market risk and interest rate risk but fail to mention that the sponsor has never completed a project of this size before. That’s material. I’ve seen PPMs for development deals that don’t adequately disclose construction cost overrun risks. That’s material. I’ve seen PPMs where the sponsor has a prior bankruptcy that isn’t disclosed. That’s definitely material—and potentially fraudulent.

If something goes wrong and an investor can argue they weren’t adequately warned, you’re exposed. The risk factors section isn’t where you undersell concerns—it’s where you demonstrate that you’ve thought through everything that could go wrong.

Conclusion

Choosing the right PPM lawyer isn’t just a legal decision—it’s a business one. You need someone who’s been in the trenches, understands syndication from the inside out, and can protect your deal without slowing it down.

I spent ten years as a litigator watching smart people destroy what they’d built. Now I spend every day helping sponsors build wealth—and protecting that wealth with legal documents designed by someone who knows exactly what’s at stake.

Don’t settle for a generalist who’s learning on your dime. Partner with a specialized attorney who’s invested in your success, and you’ll build a foundation that pays dividends across every future raise.

My fee is $15,000 for your first deal, $10,000 for repeat business, and I deliver your complete document package in days, not months. Your investors get investment-grade documents they can understand. You get protection designed by someone who protects their own deals the same way.

That’s the difference between a lawyer who studies syndications and one who runs them.

Ready to launch your Regulation D offering with documents drafted by an attorney who’s actually syndicated deals? Schedule a consultation at MoschettiLaw.com to discuss your capital raise.

Tilden Moschetti, Esq., is a highly sought-after syndication attorney with nearly two decades of experience. His clientele ranges from real estate developers and startups to established businesses and private equity funds. Tilden’s expertise in syndication law comes not only from his knowledge of syndication and securities law but from real, hands-on experience as an active syndicator himself in every real estate product type and nearly all markets in the US. His knowledge and experience set him apart and established him as the Reg D legal services leader.